The South African Rand was approaching some of its worst levels in over a year prior to the weekend, as liquidation in the Chinese Renminbi and rebound by the US Dollar derailed a multi-week rebound and sparked a ferocious decline in South African currency exchange rates.

The South African Rand was approaching some of its worst levels in over a year prior to the weekend, as liquidation in the Chinese Renminbi and rebound by the US Dollar derailed a multi-week rebound and sparked a ferocious decline in South African currency exchange rates.

On the last trading session last week, the South African Rand had lost ground against all G20 rivals for the week, as a result of pressure resulting from the People’s Bank of China’s (PBOC) unexpected interest rate drop on Monday in response to weaker-than-anticipated economic data from China for July.

“This was followed by an unexpected increase in onshore trade volumes and a lessening of negative forward values. This is congruent with FX intervention driving up spot trade volumes and depleting CNY liquidity. The consequence is that lawmakers want an orderly decline of the CNY rather than one that causes portfolio exodus” according to BofA Global Research’s chief of developing markets Asia fixed income and FX strategy, Claudio Piron.

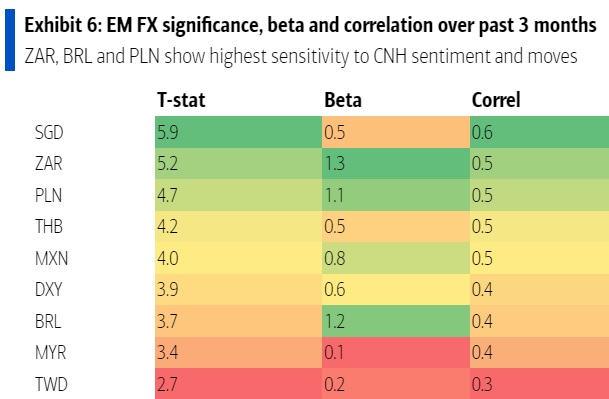

“Exhibit 6 depicts a comparison of three-month historical EM FX betas to the CNH, along with significant t-statistics and betas. Only five of the nine EM currencies have a greater beta than the DXY USD index. These include ZAR, BRL, PLN, and MXN, indicating that CNY fluctuations influence EM currencies through a mix of risk perception and trade mechanisms” Piron produced a synopsis of this week’s research papers.

China’s rebound from the recent usage of coronavirus prevention methods has been sluggish than several economists had predicted, prompting the People’s Bank of China to take action.

But China aspects were not inevitably the only drag on the South African Rand in the week leading up to Friday, as the Dollar also shored up on its own from mid-week onwards as some U.S. economic data came in more positive than anticipated and minutes of the most recent policy meeting indicated the Federal Reserve will not be effortlessly discouraged from its June plan to raise US interest rates to as high as 3.5% in 2022 and even higher in the near future.

“The market is now on the fence between 50bp and 75bp for the September FOMC meeting, with crucial activity data forthcoming in the next weeks. Our G10 team believes the USD is nearing its top but will likely stay strong for some time. In addition, China’s indicators are deteriorating once again, but we do not anticipate a major push to follow the most recent rate decrease and still envision $/CNH around 7.0 by the end of 2022. This puts EEMEA FX under stress from several directions” Piron’s macro-strategist partner at BofA, Mikhail Liluashvili, believes this.

“Our econometric theory implies that the rand is currently overpriced. Furthermore, the model anticipates that the USDZAR would peak at 17,14 in September, based on BofA’s own estimates for EURUSD, major South African export and import costs, benchmark rates in the US and South Africa, and the worldwide PMI” in addition, Liluashvili added this week.

Liluashvili and colleagues suggested earlier this week that customers sell the Rand and purchase the Dollar in expectations of a prolonged break by USD/ZAR back above 17.0. Since that day, the Dollar has nearly completely overturned four weeks of downturn that had pulled it aside from the 61.8% Fibonacci retracement of the declining trend stretching back to March 2020.

“The likelihood for a dismal Q2 GDP should stoke the flames. We anticipate the Q2 GDP to fall by 0.7% quarter-over-quarter, a decrease from our earlier forecast of flat growth. The effects of flooding in April and power outages in June will undoubtedly cause the economy to decline. This should exert some unfavorable downward pressure on the rand’s future prospects” Liluashvili also stated in connection to the South African economic data that will be released at the beginning of September.

Dollar gains and Rand losses may have also been reinforced on Thursday and Friday by the latest comments from Federal Reserve lawmakers who looked to ponder aloud and in public this week whether the Fed should choose a third consecutive 0.75 basis point rise in the US benchmark rates for September.

In the last week of July, when financial sector speculation about the perceived likelihood of a looming US recession was rampant prior to the roll out of a slew of economic findings in August indicating that the US inflationationary pressures may have mediated recently, this possibility was all but written off.